Name: Evolution AB Ticker: EVVTY

Market Capitalization: $23 billion Industry: Online Gambling Sector: Consumer Cyclical

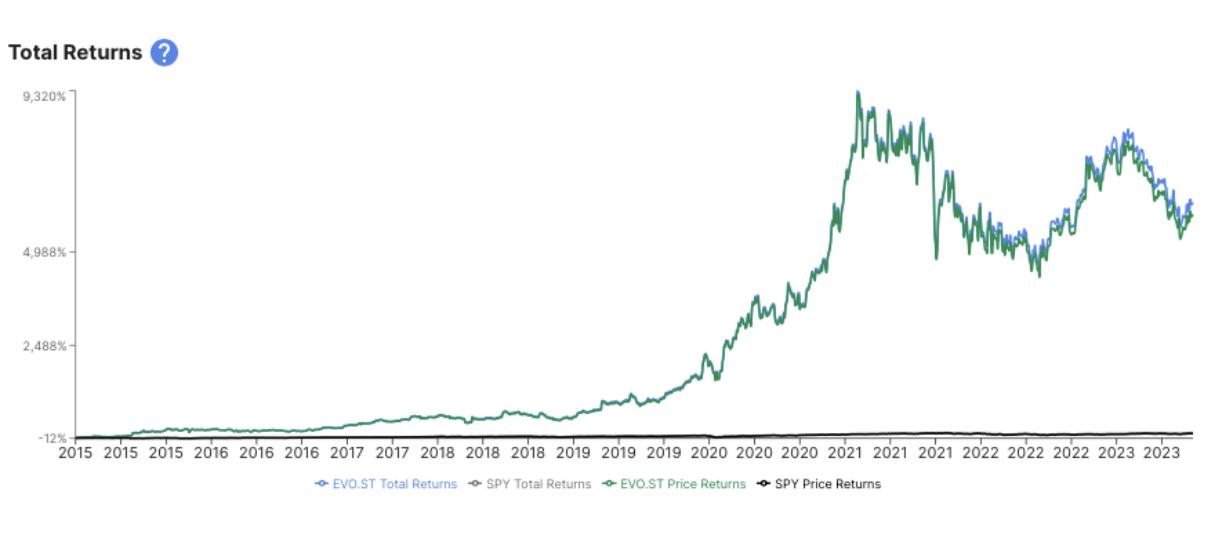

Return since IPO in 2015: 6,049% (a 62% Compounded Annual Growth Rate) |

Introduction

Evolution is a leading B2B solution provider for casino operators offering live casino, live game shows, slots and more. The company's vision is to become the leading online casino provider globally. Evolution has evolved significantly since its inception in 2006 from a rudimentary Live Casino Roulette game to a comprehensive ecosystem of Live Casino games tailored to various player preferences.

Evolution's customer base includes global online operators, platform providers, and an expanding number of land-based casinos. As of the end of 2022, the company's customer portfolio comprised over 700 customers. Notable clients include DraftKings, Paddy Power, FanDuel, MGM Resorts, and Wynn Resorts. The revenue model encompasses commission fees, live casino customization, dedicated table fees, and set-up fees for new customers. |

Historical Performance

Founded in 2006 and public since 2015, EVO has achieved an extraordinary track record. Since the IPO, the Compounded Annual Growth Rate (CAGR) of the stock has been 62%, outperforming the S&P 500 by a huge margin. |

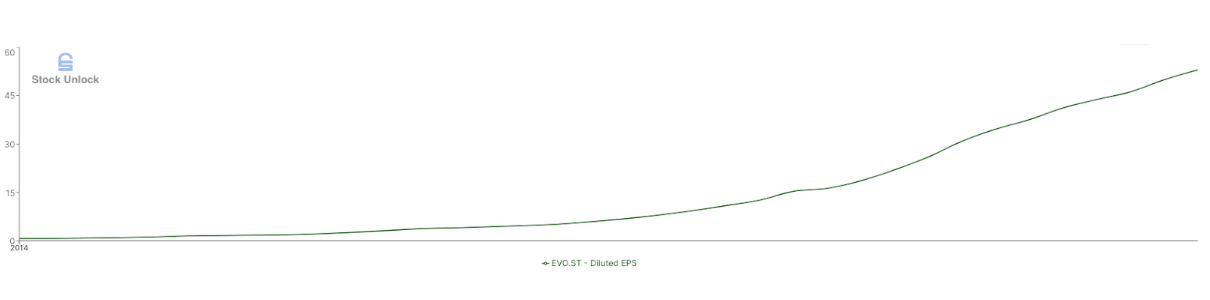

Financial Analysis Since 2015, the company has grown its revenue and earnings in an extraordinary way: - Revenue has grown at a CAGR of 50.6%.

- Net income has grown at a CAGR of 69.5%. - EPS has grown at a CAGR of 64%.

During this period, revenue has been multiplied by 32, net income by 89, and EPS by 67, as you can see in Stock Unlock's Free From Tool. You understand now why the stock has had such a spectacular return.

|

The company has notably improved operating margins from 11% (2013) to 22% (2023), reflecting increased efficiency with a Return On Invested Capital (ROIC) averaging 17%. |

Sometimes investing is that simple. EPS goes up by 60% per year, the stock goes up by 60% per year. Stock price follows EPS. Even in recent years, the company’s segments have been growing nicely. Evolution's ability to scale its games, the efficient use of live dealers, and economies of scale have improved operating margins from 22% (2015) to 63% (2023), with a Return On Invested Capital (ROIC) averaging 67% during this period.

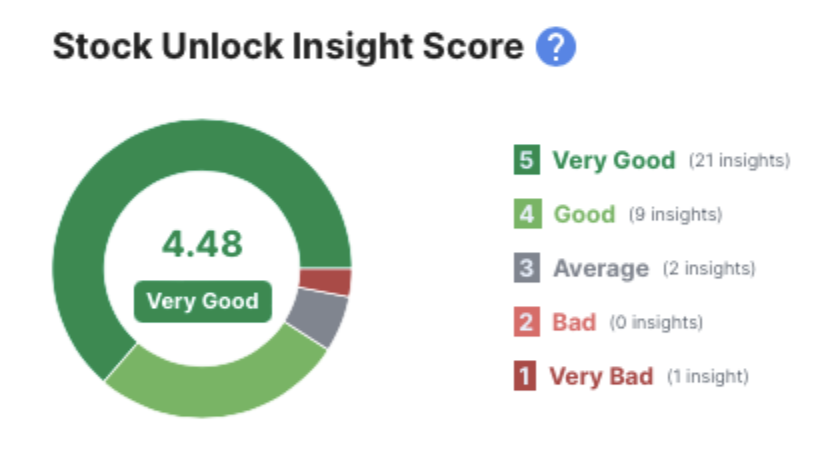

With all these good numbers, EVO has a good Stock Unlock Insights Score of 4.48. |

Balance Sheet With over €850 million in cash and zero debt, Evolution maintains an impeccable balance sheet. Its current ratio is 3 and the company generates a lot of cash flow, indicating no problem to weather short-term negative events. |

Capital Allocation The company, in its attempt to position itself as the #1 world-leading content provider, actively engages in many acquisitions to enhance its offering. The most notable acquisitions are Nolimit City in 2022 for €340M (all in cash, €200M upfront, €140M in earn-outs up to 2025), Big Time Gaming for €458M in 2021 (Cash €80M, €148M in shares and €230M in earn-outs up to 2024) and NetEnt for €2.3B in 2020 in shares.

It seems that EVO overpaid for its acquisition of NetEnt which decreased the Return On Investment Capital (ROIC) because profits did not increase proportionately to the equity they bought. Nonetheless, the acquisition was strategically important to enhance its B2B offering and to strengthen its presence in important markets like the US. The firm also pays a solid dividend with a yield at 2.1%. The company plans to pay 50% of its cash flow to dividend. As cash flows increase, we should expect more dividends in the future. |

Competitive Advantage Evolution boasts enduring competitive advantages that contribute to its leadership in the live casino market. These include: Intellectual Property Advantage: Exclusive portfolio of proprietary games like Monopoly Live and Lightning Roulette are hard to replicate; a large player base ensures cost efficiency.

Scalability: Operating digitally allows accommodating an unlimited number of players without expanding physical infrastructure, ensuring higher ROI. In traditional casinos, adding more tables and dealers would directly increase costs, but Evolution can accommodate more players without significantly increasing expenses. Since 2014, Evolution has been able to more than double revenue per live table from €404k to €914k.

Network Effects: Strong player engagement, social interaction, and a diverse game portfolio contribute to market dominance. Evolution has many games that players like, and this also brings in operators. Online casinos want to offer a lot of games, so the more games Evolution has, the more operators it can work with. This creates a better casino experience for players who can enjoy a variety of games in one place. Once players enter the Evolution ecosystem, they are more likely to stay within it.

Switching Costs: Substantial setup fees for dedicated tables (up to €50,000) and monthly fees (up to €20,000 per table) deter operators from switching providers. These fees, coupled with high margins, incentivize operators to stay with Evolution. Operators are usually locked into contracts with Evolution for three years, making it less attractive to switch to another company during that time. |

Growth Opportunities

Apart from continued innovation and efficiency, some things can improve Evolution:

Expansion of the Online Gambling Market: anticipated to reach $153.57 billion by 2030, the global online gambling market is set for substantial growth, projecting a compound annual growth rate (CAGR) of 11.7% from 2023 to 2030. This expansion is driven by factors such as widespread smartphone (highest expected CAGR from 2023 to 2030) and internet accessibility, the prevalence of freemium models, and growing cultural and legal acceptance. The Asia Pacific region is poised for remarkable growth in the years to come.

Artificial Intelligence: AI will also play a role in EVO’s growth. At the heart of their ecosystem lies an intelligent lobby, unveiled to players in 2022. Drawing inspiration from platforms such as YouTube and Netflix, it is powered by an advanced artificial intelligence (AI) recommendation engine that helps customers choose their games. Virtual Reality: VR technology is revolutionizing the online gambling experience by creating immersive environments that enable users to interact realistically with hardware, other players, and dealers, enhancing sound quality and game design. |

Risks

Regulatory risk is a notable challenge for Evolution, given its dependence on gaming laws across jurisdictions. On the other hand, this regulation risk could be an opportunity for increasing barriers to entry in the industry (think of tobacco companies or social media companies that are highly regulated and still enjoy strong competitive advantages). Additionally, the concentration of revenue from top customers and the rising workforce costs associated with expansion into the United States pose risks. The need for multiple studios due to regulatory requirements could impact economies of scale. |

Valuation is the hard part of the analysis. The company has been growing so fast, what assumption do you make? What multiple should you use for such a quality business? Let’s try our best.

Using Stock Unlock’s DCF Tool, we are able to see what sort of return investors can expect from Evolution AB over the next 5 years, assuming very conservative assumptions:

20% CAGR earnings growth (compared to 50% CAGR in the past) 3% shares outstanding growth rate (assuming more acquisitions) P/E of 20 (at the end of Year 5) If Evolution drastically slows down, and is trading at PE 20 like American indices, then the fair value of the shares is $136 or about 26% above where the stock is currently trading. |

Evolution AB is an incredible company growing fast with strong competitive advantages. You can check out all of Evolution's Stock Unlock Insights to help you get started with analyzing this business. |

This Newsletter's Author

This newsletter was written by Christophe Nour. You can find him via YouTube, Twitter, LinkedIn, and even view his portfolio on eToro.

Additionally, if you have any questions about this newsletter, you can send him an email at: christophe.nour@icloud.com |

Disclaimer:

Stock Unlock's newsletter is not a recommendation to buy or sell stocks. Stock Unlock does not provide financial advice, and we are writing this newsletter to help share ideas and teach you more about stock analysis. Please do not buy or sell stocks we discuss without doing your own research and/or consulting with a professional. |

Let us know if you have any feedback |

In addition to providing education around investing fundamentals we are exploring adding value through sending our members stock ideas and analysis. Please let us know if you enjoy this type of newsletter or have any feedback. |

|

|

|