Interested in Working With Stock Unlock? |

We have an exciting announcement! Stock Unlock is looking for someone to help us reach more people through our social media channels.

We are looking for someone who is great at social media posting, and creating content. If this is you, and you'd like an opportunity to work with Stock Unlock, then please respond to this email! |

Lessons from François Rochon’s Letters to Partners |

With an incredible track record, including massively outperforming the S&P 500 over 30 years, François Rochon is a familiar name to many investors.

Rochon’s Montreal-based firm, Giverny Capital, has delivered 14.8% compounded annual returns since 1993 - that means $100,000 invested in 1993 would have turned into just over $6.7 million by the end of 2023. Despite the spectacular numbers, Rochon’s Letters to Partners are often overlooked. The letters are a fantastic resource for investors looking to learn how one of the top investors approaches the stock market, picks stocks, and reviews management.

Let’s dive into some of the key lessons from François Rochon: |

1. Even the Best Investors Makes Mistakes |

One of the most unique features of Rochon’s letters is the fact that every annual letter ends with a “Podium of Errors” section. In this section, Rochon discusses three mistakes he and Giverny Capital have made over the years. The mistakes are not always “we sold too early” types, but rather what lessons investors can draw from the errors. In the most recent letter, Rochon mentions selling Brown & Brown back in 2009 due to doubts about the founder’s succession plans and because the market presented better opportunities elsewhere. Regardless, the big lesson is in Rochon’s conclusion that his mistake was to stop following the company after initially selling:

“I don’t think selling the stock in 2009 was a mistake. What was a mistake was to stop following the company. I could have noticed the improvement in Brown & Brown’s business fundamentals,” (2023 Letter).

|

2. Partner with Quality Management |

“A franchise doesn’t emerge from nowhere. It is built by men (or women). The essential ingredient thus is the quality of top management. Becoming shareholder is becoming partner with them,” (2003 Letter).

Firstly, the word franchise is taken directly from how Warren Buffett describes a company with inherent qualities that protect it from competitors (in other words, a moat). That gives you an idea of to what extent Buffett and Berkshire Hathaway inspire Rochon’s investment philosophy.

Furthermore, Rochon repeats in each annual letter that a long-term investment horizon is fundamental to Giverny Capital. That makes it increasingly important to invest with honest management in terms of alignment and skin in the game. After all, if a management team is not incentivized to create long-term value for shareholders, why should investors partner with them?

Rochon’s focus on quality and integrity goes beyond just his investments; Giverny Capital also refers to their clients as “partners” as a reminder to clients and portfolio managers that they are in the same boat. |

3. Have (at least) a 5-year investment horizon |

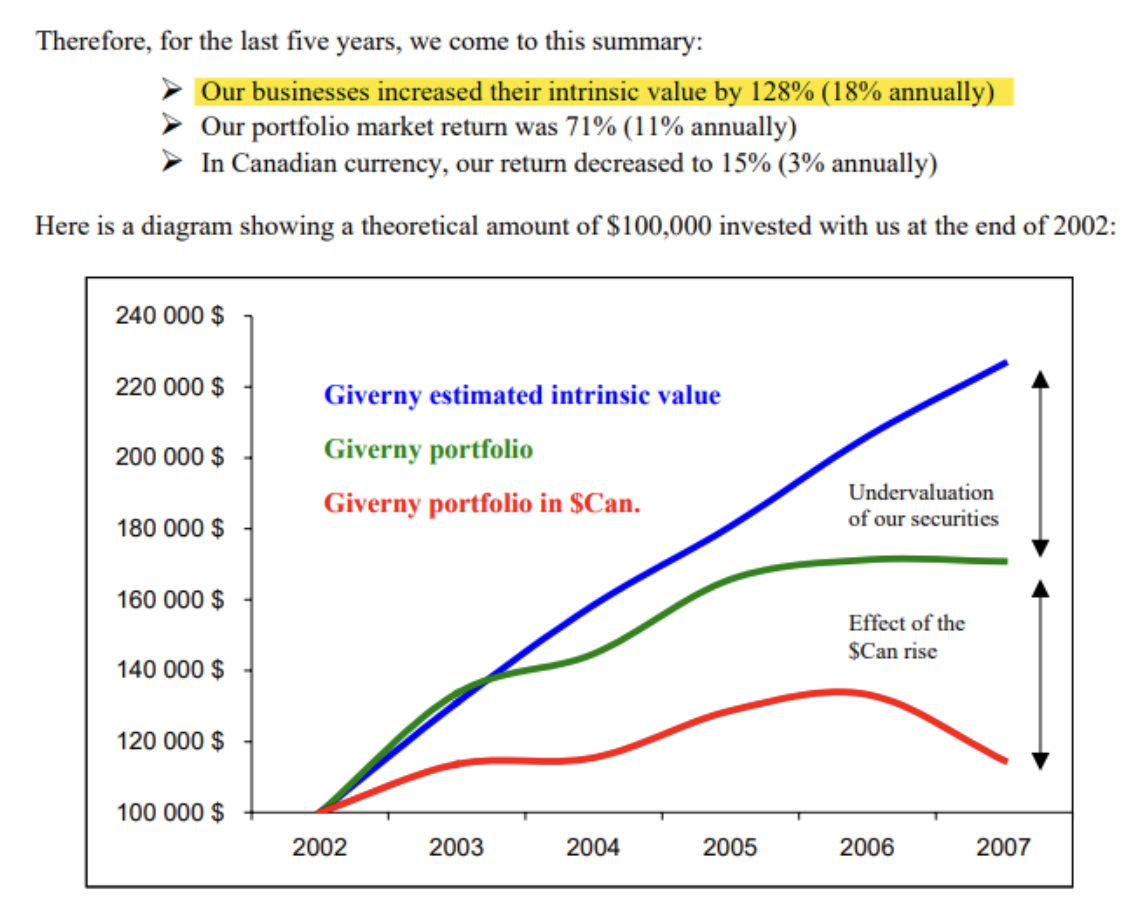

Similar to the “Podium of Error” tradition, Rochon started doing a five-year postmortem review all the way back in 2002. Inspired by Johnson & Johnson, which performs a similar postmortem review five years after an acquisition, the idea is to go back five years to look at the decisions that were made and the outcomes of those decisions.

Rochon typically reviews his portfolio sales and whether his reasoning behind those sales was correct. However, he also reviews his fund’s performance from time to time. In 2007, Giverny Capital had underperformed the S&P 500 over the five-year period from 2003 to 2007 due to valuation multiple compression and currency fluctuations between U.S. and Canadian dollars.

While valuation multiples and currencies will fluctuate with the market, Rochon focuses on the intrinsic value of the companies in his portfolio. Even though the stock price returns were lackluster, Giverny’s positions had more than doubled their intrinsic values (measured by earnings growth + dividend yield) over the past five years. And as we know, Giverny has returned significantly in excess of the S&P 500 since inception - despite years of underperformance.

|

4. Stop Trying to Predict the Market |

“I would like to emphasize the most important lesson of the last twenty years: It is futile to try to predict the stock market over the short run. All previous lessons are useless if you try to predict the stock market over the short run. Owning great businesses, managed by great people and acquired at reasonable prices is the winning recipe. The rest is just noise,” (2013 Letter)

Since Giverny Capital was founded in 1993, the stock market has suffered through recessions following the dot-com bubble in 2000 and the global financial crisis from 2008 to 2009, as well as steep declines in September 2001 and March 2020, among several more. Yet, the S&P 500 has returned more than a 9% compounded annual growth rate over the past 30 years. Returns are never linear, and short-term results are just as much about luck as skills. Even the best money managers underperform the index. That makes patience an essential skill for investors so that the market, over time, can recognize the true value of the best companies. |

5. Investing is Not a Game |

“Investing in the stock market is about acquiring partial ownership in companies. It is not a game. Those who approach the market as if it were a casino end up with the results of gamblers,” (2013 Letter).

A chunk of the stock market’s participants treats investing like gambling. Rochon argues that this is to the advantage of the long-term investor because it allows, at times, great businesses to trade at prices well below intrinsic value. This echoes Benjamin Graham’s Mr. Market allegory, which the intelligent investor knows how to exploit. When investors understand that stocks represent ownership in a business, they focus more on the company's intrinsic value than the stock price. And in the long run, intrinsic value growth will be the primary driver of stock returns. |

Conclusion

François Rochon has built an incredible track record over more than 30 years of investing, making all of his letters a worthy read. Fascinatingly, Rochon’s investment philosophy is anything but complicated. In addition to continuously emphasizing the importance of quality management and taking a long-term approach to investing, the same themes re-occur throughout his letters:

- Embrace and learn from your mistakes. Even the best investors make errors. Writing and reviewing past mistakes is an excellent way to avoid repeating them.

-

If you have found a great business trading at a reasonable price, don’t worry about what interest rates will be in a year or what the market will do next.

-

Remember that buying a stock is buying a small piece of a business. It is not a piece of paper to be traded back and forth. Focus on the intrinsic value of your business; everything else is noise.

|

This Newsletter's Author This newsletter was written by Jørgen Pettersen. You can find him on Twitter/X. |

Disclaimer:

Stock Unlock's newsletter is not a recommendation to buy or sell stocks. Stock Unlock does not provide financial advice, and we are writing this newsletter to help share ideas and teach you more about stock analysis. Please do not buy or sell stocks we discuss without doing your own research and/or consulting with a professional. |

Let us know if you have any feedback

In addition to providing education around investing fundamentals we are exploring adding value through sending our members stock ideas and analysis. Please let us know if you enjoy this type of newsletter or have any feedback. Let us know what you think by emailing support@stockunlock.com |

|

|

|